Japan Credit Scores: The Expat Guide to CIC, JICC, and JBA Reports

Unlike in the US or UK, Japan does not use a single credit score. Learn how the three credit bureaus track your financial history and how expats can check their reports.

YenWise Editorial

Japan personal-finance research for expats

If you are applying for a credit card, a mobile phone contract, or a home mortgage in Japan, you might wonder: "What is my credit score?" Unlike in countries like the US, UK, or Canada, Japan does not use a single, standardized credit score (like a FICO score) that you can easily lookup. Instead, creditworthiness is assessed by reviewing detailed reports from three separate credit bureaus.

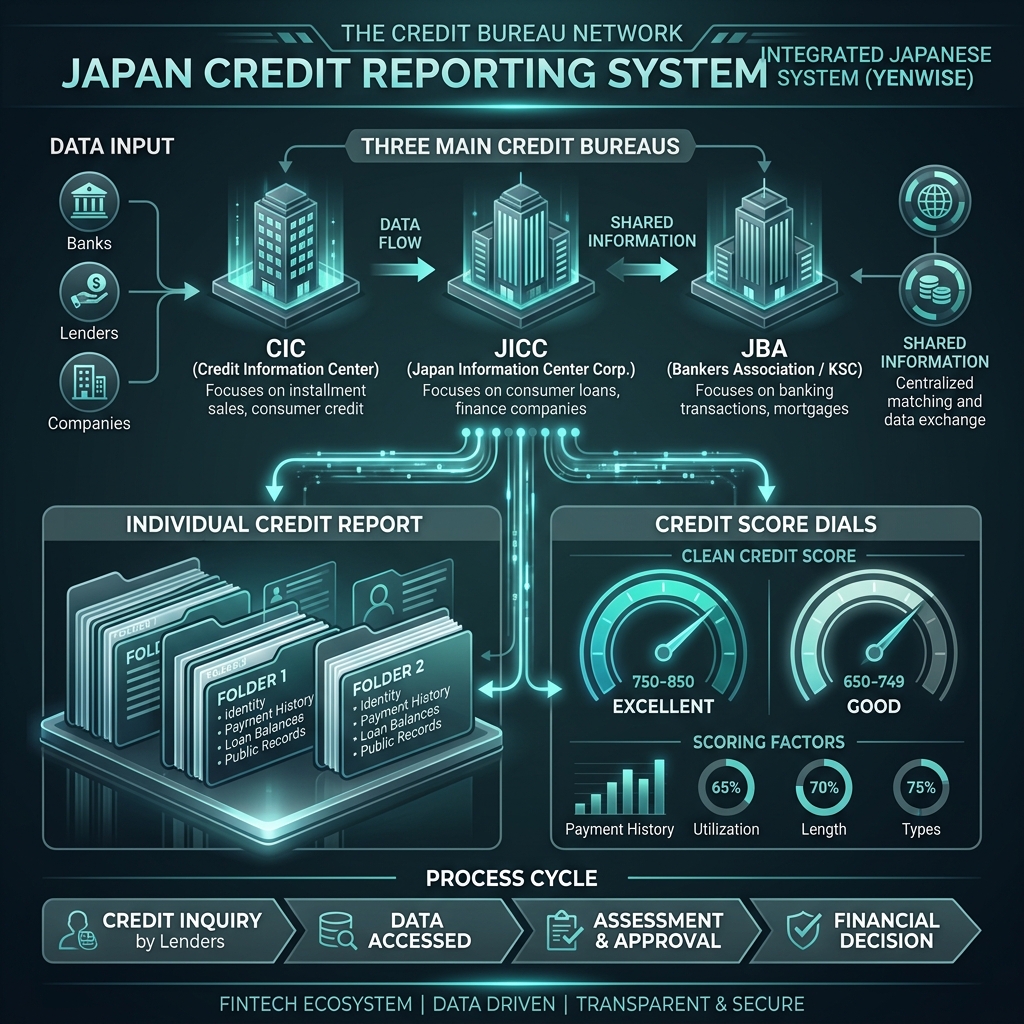

The Three Main Credit Bureaus in Japan

Every financial institution in Japan is affiliated with one or more of the three primary credit information agencies (信用情報機関). These agencies collect data on your loans, credit card usage, and installment contracts:

- CIC (Credit Information Center): Mainly used by credit card companies and consumer finance companies. If you have a credit card or are paying off a smartphone in monthly installments, your data is here.

- JICC (Japan Information Center Corp.): Focuses primarily on consumer finance loans, credit cards, and retail installment credit.

- JBA / KSC (Japanese Bankers Association / Bankers Association Credit Information Center): Administered by commercial banks and shinkin banks. This is the primary bureau checked during mortgage applications.

How Expats Can Request a Credit Report

Under Japanese law, you have the right to request a disclosure of your own credit records (自己開示). Both JICC and CIC allow you to request your report online (via a smartphone app), by mail, or in person. Each report costs approximately ¥1,000 to disclose. JBA (KSC) reports must be requested by mail or online.

What Factors Affect Your Japanese Credit Report?

Instead of a score, your report contains a history of your monthly payments marked with symbols: - $ (Dollar sign): Paid in full and on time. This is the ideal symbol. - P (Partial): Paid only partially. - R (Receipt): Paid by a third-party guarantor. - A (Arrears): Unpaid/late payment. Having an "A" on your report is a red flag that can prevent card or loan approval.

Key factors that damage your creditworthiness in Japan include:

- Delinquencies (延滞): Payments delayed by more than 61 days or 3 months are marked as a serious default (異動) and stay on your record for 5 years.

- Multiple card applications (多重申込み): Applying for 3 or more credit cards in a short period indicates financial distress. Application history is kept for 6 months.

- Mobile phone contract defaults: Missing a payment on a subsidized mobile phone plan counts as a credit default. This is the most common reason young expats are denied credit cards.

For official procedures, you can visit the disclosure portals of JICC and CIC.