Japan Inheritance Tax: A Complete Guide for Expats and Foreign Residents

Japan's inheritance tax can reach 55% — among the highest in the world. Learn how the basic deduction, tax rates, and 10-year rule affect expats receiving inheritances from abroad.

YenWise Editorial

Japan personal-finance research for expats

Japan has one of the highest inheritance tax rates in the developed world, with a top marginal rate of 55%. For expats and foreign residents, the rules are particularly complex because they depend on your visa type, how long you have lived in Japan, and where the deceased and their assets were located.

Who Is Liable for Japanese Inheritance Tax?

Three categories of people can be liable for Japanese inheritance tax on assets received from a deceased person: 1. Unlimited taxpayers: Japanese citizens and Table 2 visa holders (spouse, PR, long-term resident) who have lived in Japan — taxed on worldwide inherited assets. 2. Limited taxpayers: Table 1 visa holders (work, student) who have lived in Japan for less than 10 years — taxed only on assets located in Japan. 3. 10-year residents: Table 1 visa holders who have lived in Japan for 10+ years out of the last 15 — taxed on worldwide inherited assets.

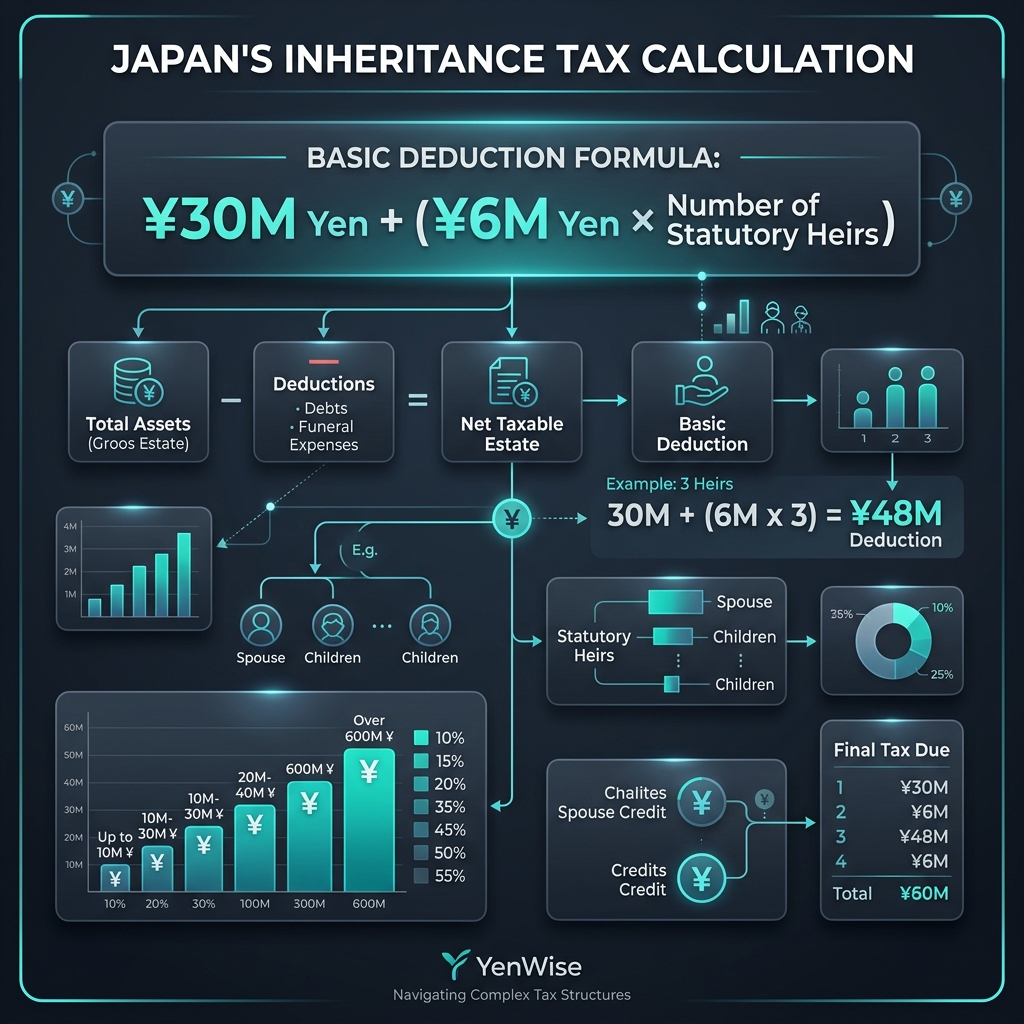

The Basic Deduction: How Much Is Tax-Free

Japan provides a substantial basic deduction before inheritance tax applies: Basic Deduction = ¥30 million + (¥6 million × number of statutory heirs) For example, if a deceased person leaves assets to a spouse and two children (3 statutory heirs), the deduction is: ¥30M + (¥6M × 3) = ¥48 million tax-free. Any inheritance above this amount is subject to tax at progressive rates.

Inheritance Tax Rates (2026)

- Up to ¥10M: 10%

- ¥10M – ¥30M: 15% (minus ¥500,000 deduction)

- ¥30M – ¥50M: 20% (minus ¥2,000,000 deduction)

- ¥50M – ¥100M: 30% (minus ¥7,000,000 deduction)

- ¥100M – ¥200M: 40% (minus ¥17,000,000 deduction)

- ¥200M – ¥300M: 45% (minus ¥27,000,000 deduction)

- ¥300M – ¥600M: 50% (minus ¥42,000,000 deduction)

- Over ¥600M: 55% (minus ¥72,000,000 deduction)

Overseas Inheritances: What Gets Taxed

If you are an unlimited taxpayer (or a 10+ year Table 1 holder) and inherit assets from a family member overseas, Japan taxes only the portion you receive — not the entire overseas estate. The basic deduction (¥30M + ¥6M × statutory heirs) applies to the entire estate, and your share is calculated proportionally.

For example: if a parent in the US leaves a $2M estate to you and one sibling, and there are 2 statutory heirs, the deduction is ¥30M + (¥6M × 2) = ¥42M. Your half of the estate is $1M (≈¥140M). Your taxable amount = ¥140M − (¥42M ÷ 2) = ¥119M. The tax on that could exceed ¥40M at the top rates.

Tax Treaties and Foreign Tax Credits

Japan has inheritance tax treaties with the United States, United Kingdom, France, and a few other countries. These treaties prevent double taxation — if you pay inheritance tax in the deceased's country, you can claim a foreign tax credit against your Japanese inheritance tax liability. However, the credit is limited to the Japanese tax attributable to the foreign assets.

For official details, visit the NTA Inheritance Tax Guide and review Japan's inheritance tax treaties.