Best Investment Accounts in Japan for Expats: SBI vs. Rakuten vs. Monex

Looking to start investing in Japan? Compare the top online brokerages (SBI, Rakuten, Monex), understand taxable vs. tax-free accounts, and navigate US expat rules.

YenWise Editorial

Japan personal-finance research for expats

Starting your investment journey in Japan can feel daunting, especially with the language barrier and complex tax structures. However, setting up a brokerage account is one of the most impactful steps you can take for your long-term financial health. In Japan, online brokerages (ネット証券 — Net Shoken) offer the lowest fees and the widest selection of investment products.

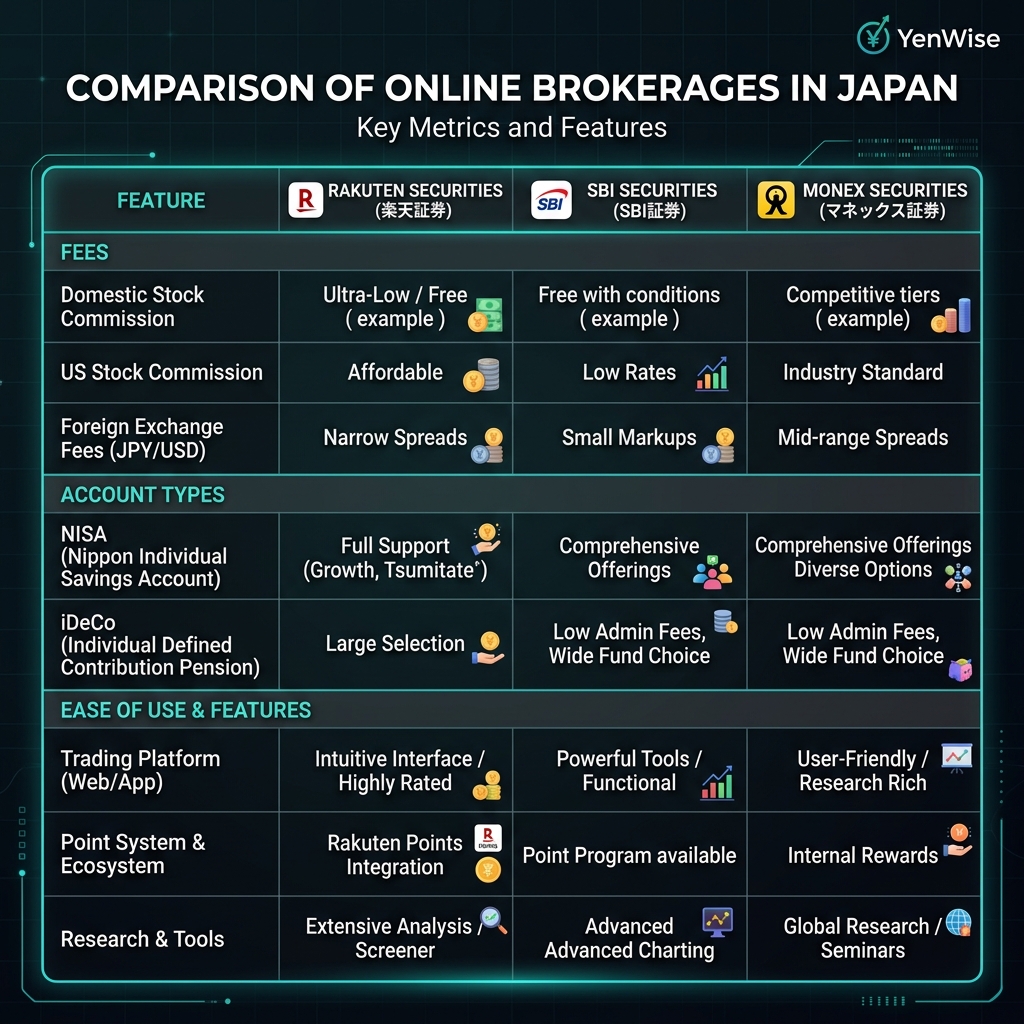

The "Big Three" Online Brokerages

Three online brokerages dominate the Japanese market. While none of them offer a native English interface, they are highly popular among expats due to low costs and ease of use with web translation tools:

- SBI Securities (SBI証券): The largest online broker in Japan by assets. It offers zero-commission trading for domestic stocks and a massive selection of mutual funds. Its interface can be cluttered, but it is highly reliable.

- Rakuten Securities (楽天証券): Known for having the most modern and user-friendly interface. It integrates perfectly with the Rakuten ecosystem, allowing you to earn and spend Rakuten Points on investments.

- Monex Securities (マネックス証券): A strong competitor that offers excellent tools for US stock trading and is popular for its integration with the d-Point and Monex card point systems.

Comparing SBI, Rakuten, and Monex

Here is a quick breakdown of how the major online brokers compare for foreign residents:

- SBI Securities: Best for low fees and product variety. English support is unavailable. NISA and iDeCo support is excellent.

- Rakuten Securities: Best for user interface and point integration. English support is unavailable. NISA and iDeCo support is excellent.

- Monex Securities: Best for US stock tools and research. English support is unavailable. NISA and iDeCo support is excellent.

Choosing the Right Account Type

When opening a brokerage account, you will be prompted to choose between different account types. It is crucial to select the correct one:

- Tokutei Koza (特定口座 — Designated Account): Always choose "Withholding Tax" (源泉徴収あり — Gensen Choshu Ari). Under this option, the brokerage automatically calculates and deducts the 20.315% capital gains and dividend taxes, meaning you do not need to file a tax return for your investments.

- NISA (少額投資非課税制度): The tax-free investing account. Capital gains and dividends are 100% tax-exempt. You can invest up to ¥3.6 million per year, with a lifetime limit of ¥18 million.

- iDeCo (個人型確定拠出年金): The private pension account. Contributions are fully tax-deductible, growth is tax-free, and payouts are taxed favorably at retirement.

The US Expat PFIC Trap

If you are a US citizen, you face severe restrictions due to US tax laws. Japanese mutual funds (including those inside NISA or iDeCo) are classified as Passive Foreign Investment Companies (PFICs) by the IRS. PFICs trigger punitive US tax rates and extremely complex reporting requirements. Consequently, US citizens should generally avoid buying Japanese mutual funds. Many US expats choose to use Interactive Brokers (IBKR) Securities, which allows US citizens living in Japan to buy US-domiciled ETFs and stocks directly, avoiding the PFIC trap.

How to Open an Account as a Foreigner

To open an account, you will need to provide:

- Your Residence Card (在留カード) with at least 3-6 months remaining validity.

- Your My Number Card (マイナンバーカード) or a Juminhyo (residence certificate) showing your My Number.

- A Japanese bank account in your exact name (matching your residence card).

To begin, check the official registration pages for SBI Securities, Rakuten Securities, or Monex Securities.

Choosing a brokerage stack as an expat

Most long-term investors in Japan combine a taxable specific account (特定口座) with tax-advantaged wrappers: new NISA for flexible investing and optionally iDeCo for deductible retirement savings. Non-residents and people leaving Japan face account closure or restriction rules that differ by broker — read the English FAQ before you transfer large sums.

Tax drag and why wrappers matter

Capital gains and dividends in taxable accounts are generally taxed around 20.315% when realized or paid. NISA removes that drag inside contribution limits; iDeCo adds an upfront deduction but locks funds until 60. Run both the NISA Calculator and iDeCo Calculator before you lock a monthly savings rate.