Japan's New NISA: How Expats Can Invest Completely Tax-Free

Japan's New NISA lets you invest up to ¥18 million completely tax-free. Here's how it works, who qualifies, and how to maximize your returns as an expat.

YenWise Editorial

Japan personal-finance research for expats

Japan's New NISA (少額投資非課税制度), launched in January 2024, is one of the most generous tax-free investment accounts in the world. It allows residents of Japan to build long-term wealth by investing in mutual funds, ETFs, and individual stocks without paying any Japanese tax on capital gains or dividends.

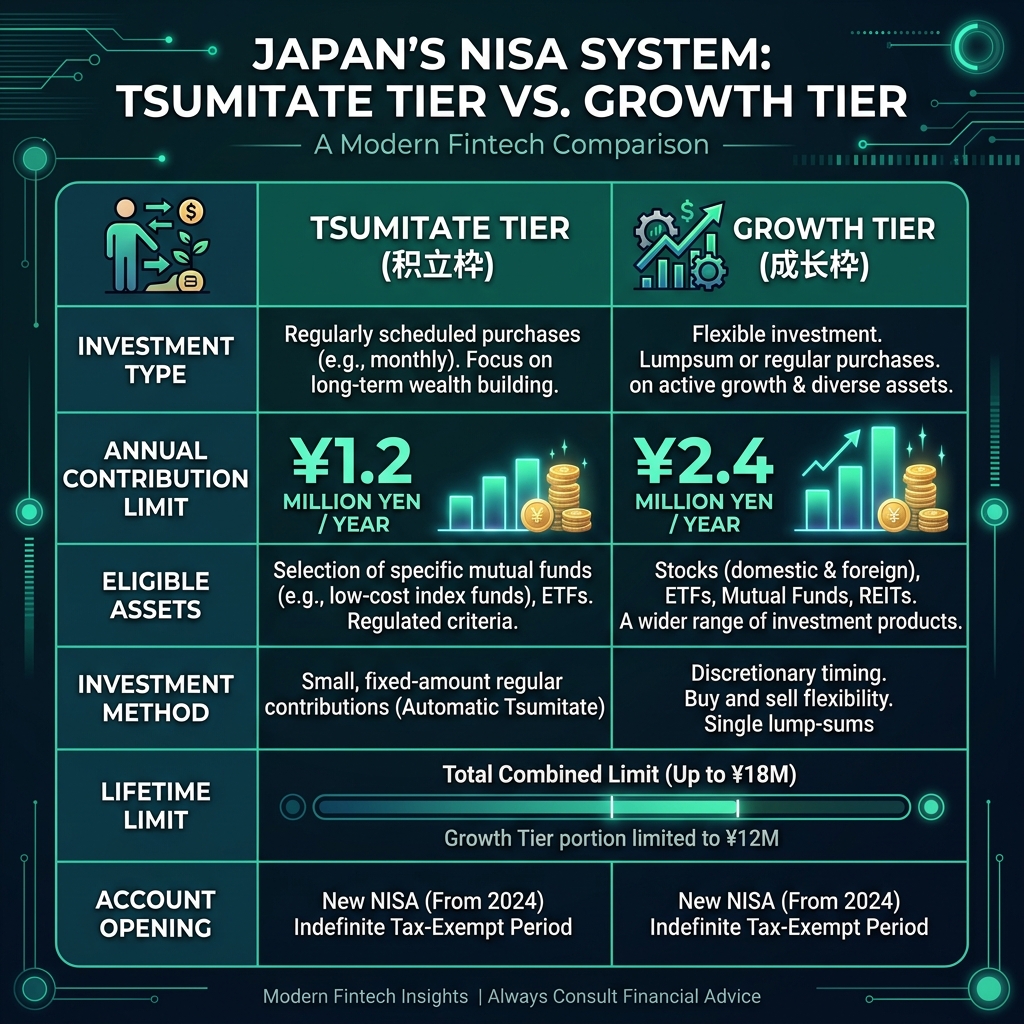

The Two NISA Tiers

The New NISA program is split into two distinct tiers: the Tsumitate Investment Tier and the Growth Investment Tier. These two tiers operate under different rules but can be used simultaneously by the same investor to maximize their annual tax-free contributions.

- Tsumitate Investment Tier (積立投資枠): ¥1.2M/year. For regular monthly investing via approved mutual funds, designed for long-term wealth accumulation.

- Growth Investment Tier (成長投資枠): ¥2.4M/year. For lump-sum investing in individual stocks, ETFs, and a wider range of mutual funds.

Lifetime Limits and the ¥18 Million Cap

The combined lifetime limit for the New NISA is ¥18 million, of which up to ¥12 million can be allocated to the Growth Investment Tier. The Tsumitate tier does not count against the Growth limit, meaning you can choose to fill the entire ¥18 million using only the Tsumitate tier if you prefer.

Who Qualifies? Expat Eligibility

Any resident of Japan aged 18 or older with a My Number card can open a NISA account. This includes expats on work visas, spouse visas, and permanent residents. Learn more about Japan's residence status on the Immigration Services Agency website.

How Much Could You Save?

Let's run the numbers. If you invest ¥100,000/month for 20 years at a 5% average annual return, use our NISA Calculator to see the difference between a tax-free account and a taxable account:

- NISA account: ¥100K/month × 20 years × 5% → approximately ¥41.1 million, ALL tax-free

- Regular taxable account: Same investment → approximately ¥37.4 million after 20.315% capital gains tax

- Tax savings: ~¥3.7 million

What Happens If You Leave Japan?

If you leave Japan permanently, you must close your NISA account. You can sell all holdings tax-free before departure and transfer the proceeds abroad. There is no penalty for early withdrawal. However, once you're no longer a resident, you cannot make new contributions.

NISA vs iDeCo: Which Should You Use?

Both are excellent tax-advantaged accounts, but they serve different purposes. NISA is flexible (withdraw anytime, no penalty). iDeCo locks funds until age 60 but offers immediate income tax deductions. Many expats use both — NISA for medium-term goals, iDeCo for retirement. Read our iDeCo guide for a full comparison.

Getting Started

- Open a securities account with a Japanese broker (Rakuten Securities, SBI Securities, or Monex)

- Apply for a NISA account during account opening (check the NISA box)

- Wait for approval (typically 1-2 weeks)

- Set up a monthly tsumitate (積立) order for automated investing

- Check your NISA usage dashboard annually to track your remaining allowance