How Much Money Do You Need to Retire in Japan? A Practical Guide

Nenkin alone won't be enough. Here's how to calculate your retirement number in Japan — factoring in pension benefits, living expenses, and the 4% safe withdrawal rule.

YenWise Editorial

Japan personal-finance research for expats

"How much do I need to retire?" is the million-dollar question — or rather, the hundred-million-yen question in Japan. The answer depends heavily on your lifestyle, your expected pension benefits, and whether you plan to stay in Japan permanently or return home.

Start With Your Retirement Expenses

The first step is estimating your monthly spending in retirement. A frugal couple in Japan with a paid-off home might live on ¥250,000–300,000 per month. A more comfortable lifestyle with travel and dining out might require ¥400,000–500,000. According to Japan's Ministry of Internal Affairs, the average retired couple spends approximately ¥260,000 per month on basic living expenses.

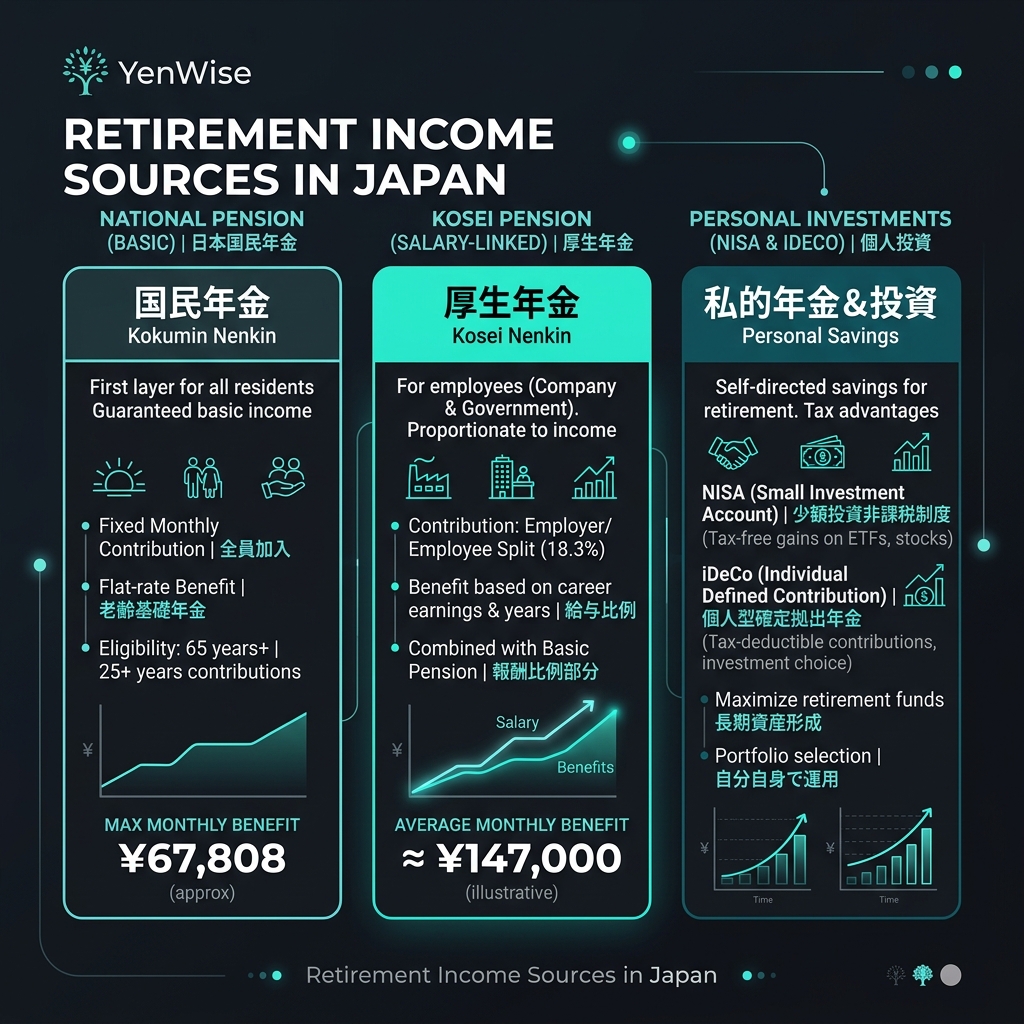

What Will Nenkin Provide?

The Japanese national pension provides a foundation, but it is modest. The full Kokumin Nenkin (basic pension) pays about ¥68,000/month (2026 figure) after 40 years of contributions. Kosei Nenkin (employees' pension) adds an earnings-related component — a typical full-career employee might receive ¥150,000–200,000/month total (basic + earnings-related).

For a couple where one spouse worked full-time and the other was a dependent, total household nenkin might be ¥200,000–250,000/month. That covers a basic lifestyle but leaves little room for travel, hobbies, or surprises.

The 4% Rule: How Much You Need to Save

The 4% rule (or safe withdrawal rate) is a widely used guideline: you can withdraw 4% of your investment portfolio in the first year of retirement, adjusted for inflation each year, with a high probability of not running out of money over 30 years.

Here is how to calculate your retirement number: 1. Estimate your monthly shortfall: Desired monthly spending − Expected monthly nenkin 2. Annual shortfall = Monthly shortfall × 12 3. Required portfolio = Annual shortfall ÷ 0.04 (the 4% rule) Example: If you need ¥500,000/month but receive ¥200,000 in nenkin, your shortfall is ¥300,000/month = ¥3,600,000/year. You need ¥3,600,000 ÷ 0.04 = ¥90 million in investments.

How to Build Your Retirement Portfolio

Japan offers several tax-advantaged investment accounts that can help you build retirement savings faster: - [NISA (少額投資非課税制度)](/en/tools/nisa-calculator): Tax-free investing with up to ¥3.6M/year in contributions. Use our NISA Calculator to project your returns. - [iDeCo (個人型確定拠出年金)](/en/tools/ideco): Tax-deductible retirement contributions with tax-free growth. Contributions reduce your taxable income. - Taxable accounts: Standard brokerage accounts. Capital gains taxed at 20.315% but only when you sell (deferred taxation).

What If You Leave Japan Before Retirement?

If you leave Japan permanently before reaching retirement age, you can claim a [Pension Lump-Sum Withdrawal](/en/tools/pension-lump-sum) of up to 5 years of contributions. You can also liquidate your NISA and iDeCo accounts (iDeCo has restrictions for non-Japanese residents). Plan ahead — your retirement strategy changes significantly if you may not retire in Japan.

For official pension projections, log into Nenkin Net or check your annual nenkin postcard. For investment planning, see the FSA's NISA page.